Over the past several years, banks have gradually adjusted their fee structures in response to digital banking shifts, rising operational costs, and increased regulatory compliance expenses. While these changes apply broadly to all customers, older account holders can sometimes feel the impact more strongly, particularly if they rely on in-person banking or traditional account types.

Many of these changes are not widely publicized, and they often appear quietly in updated fee schedules or account agreements. Understanding them can help customers avoid unnecessary charges and better manage their finances.

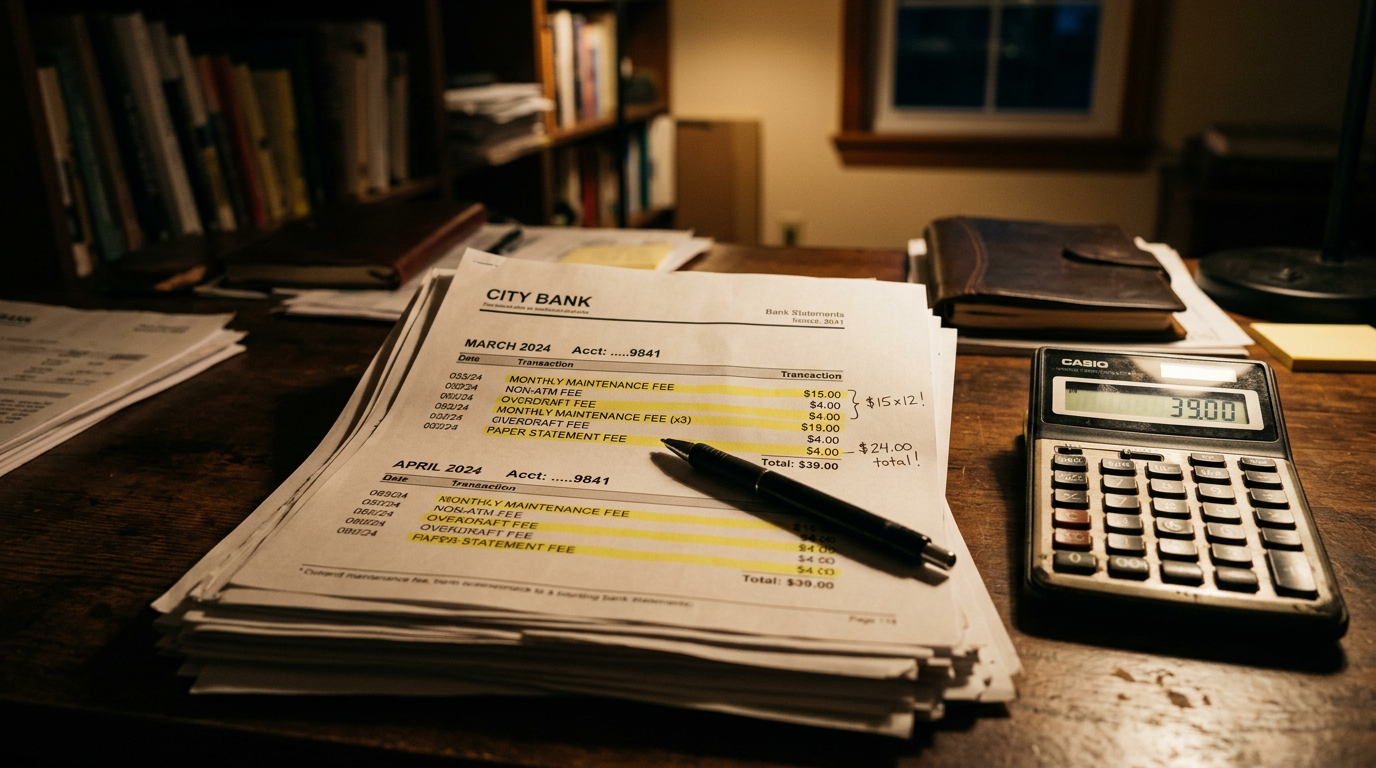

Higher Monthly Maintenance Fees On Basic Accounts

Bank of America and other major banks have gradually increased monthly maintenance fees on standard checking accounts over time, especially for accounts that do not meet minimum balance or direct deposit requirements.

For customers who prefer keeping lower balances or using paper statements, these fees can add up quickly. While digital banking customers may avoid some charges through online-only account structures, traditional account holders are more likely to encounter these maintenance costs.

Paper Statement And Mail Processing Fees

Many banks now charge extra for printed monthly statements or mailed account summaries. This shift is part of a broader push toward digital banking, but it can impact customers who are less comfortable with online-only systems.

Wells Fargo, for example, has implemented or adjusted fees in certain account tiers related to paper statements and physical document requests.

These charges may seem small individually, but over time they can become a recurring cost for those who prefer or require physical records.

ATM Fee Increases And Out-Of-Network Charges

ATM fees have steadily risen, especially when using machines outside a bank’s network. Customers can now face charges from both their own bank and the ATM operator, leading to double fees per transaction.

Chase customers, like those at many large banks, may encounter higher out-of-network ATM fees depending on account type and location.

This is particularly impactful for individuals who rely on cash and prefer in-person withdrawals rather than digital payments.

Account Inactivity And Dormancy Fees

Some banks now impose fees on accounts that remain inactive for extended periods. These “dormant account” charges are designed to offset administrative costs for maintaining unused accounts.

Older customers who maintain multiple accounts or travel for extended periods may be more likely to encounter these fees without realizing their account status has changed.

Common triggers include:

- No deposits or withdrawals for several months

- Lack of online login activity

- Unlinked or unused savings accounts

- Forgotten secondary accounts from previous banking relationships

Increased Fees For Human Teller Services

As banks encourage digital banking, some institutions have introduced or increased fees for services performed at physical branches, such as cashier-assisted transfers or paper check processing.

Citibank and similar institutions have increasingly prioritized digital channels, sometimes making in-person services less cost-efficient or subject to higher fees.

This shift can disproportionately affect customers who prefer or need face-to-face banking assistance.

Rising Minimum Balance Requirements To Avoid Fees

Many banks have increased the minimum balance thresholds required to avoid monthly service fees. Customers who fall below these thresholds may be charged regardless of account usage.

This change can be challenging for individuals on fixed incomes or those who keep smaller balances for budgeting purposes. Even modest fluctuations in account balances can now trigger penalty fees that were less common in earlier banking models.

Conclusion

Bank fee structures continue to evolve as financial institutions adapt to digital-first operations and changing economic conditions. While these changes are not targeted at any specific group, they can affect customers differently depending on how they bank. Staying aware of account terms, reviewing monthly statements carefully, and asking banks about fee-free account options can help reduce unexpected charges and improve long-term financial management.

Leave a Reply